Income Tax For Foreign Nationals In India

In India, an individual’s income is taxed at graduated rates, depending on his/her residential status in India, as determined by the Income Tax Act, 1961 and income level. Non-employment income is taxed at a variable rate according to income type.

In this article, we outline the rates and calculation methods for both income sources, and summarize common tax deductions and inclusions in income for foreign nationals working in India.

Who Is A Foreign National In India?

Any individual who is not a citizen of India is considered a foreign national.

However, whether a foreign national is liable to pay Indian income tax is dependent on the individual’s physical presence in India during a financial year which runs from April 1 to March 31, regardless of their citizenship or the purpose of the stay.

Residential Status And Tax Liability Under Income Tax Act, 1961

Residential Status

Section 6 of the Income Tax Act, 1961 defines the principles governing an individual’s residential status in India.

- Resident: An individual is said to be “resident” in India if they qualify either of the following conditions.

-

- They are present in India in the relevant fiscal/tax year for a period of 182 days or more; or

- They are present in India for a period of 60 days or more during the relevant fiscal year and a total of 365 days or more during the four fiscal years immediately preceding the relevant fiscal year.

-

Resident and ordinarily resident (ROR): If an individual qualifies the following two conditions, they will be deemed as ordinarily resident.

- The individual has been “resident” in India in at least two out of the 10 fiscal years immediately preceding the relevant fiscal year; and

- The individual’s stay in India during the seven preceding fiscal years immediately preceding the relevant fiscal year is 729 days or more.

- Resident but not ordinarily resident (RNOR): If the individual qualifies as a resident only based on the deemed residency clause or based on the reduced stay of 120 days or more, and does not satisfy any other basic condition, they will be qualified as an RNOR.

- Non-resident (NR): If none of the conditions specified for residency are met, then the individual will qualify as a non-resident.

Tax Liability Of Foreign Nationals

- Resident but not ordinarily resident (RNOR): These individuals are taxed on their worldwide income.

- Resident and ordinary resident (ROR): These individuals are taxed on their income sourced or received from India, or from an income derived from a business set up or controlled in India.

- Non-resident (NR): These individuals are not liable to income tax.

Tax Calculation

Total income tax is calculated in accordance with the tax rates and rules that stand on the first day of April of the assessment year.

Income earned in a year is taxable in the next year. The year in which income is earned is known as the financial year, while the next year in which income is taxable is known as the assessment year.

Employment income includes all amounts, either in cash or in kind, that arise from an individual’s employment. Wages, pensions, bonuses, commissions, perquisites in lieu of salary, reimbursement for personal expenses, securities or sweat equity shares, contributions to superannuation funds, etc. are all included in employment income.

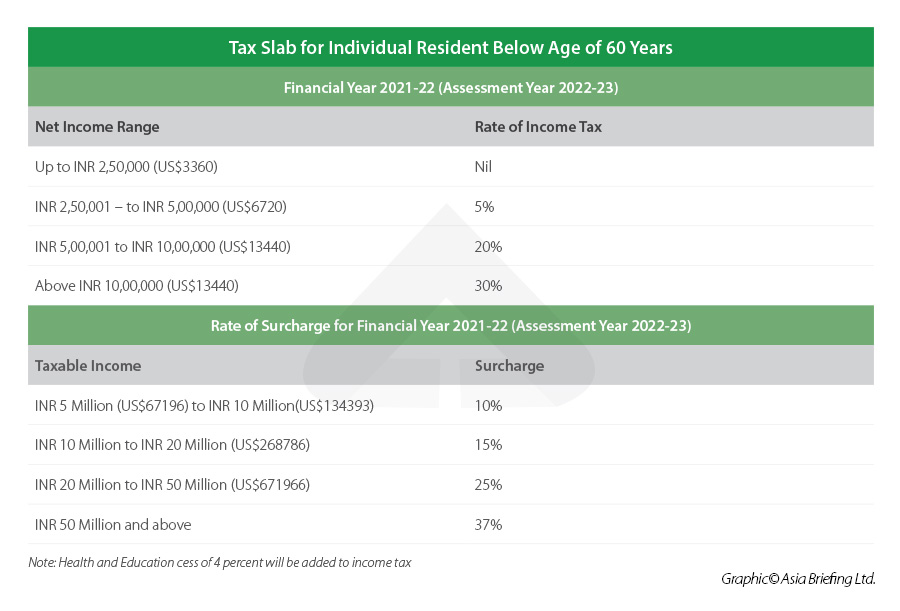

Taxation Under The Old Tax Regime

Employment Income

India provides that certain perquisites and allowances must also be included in employment income. Perquisites and allowances are taxed differently under Indian law. Limited deductions from income also exist.

Perquisites

A perquisite is any benefit received by the employee that is in addition to salary. Perquisites increase taxable income. In general, the taxable value of the perquisites to the employee is their cost to the employer. However, India has given specific rules for the valuation of the following perquisites provided by the employer:

- Residential accommodations;

- Motor car;

- Utilities;

- Free or concessional educational facilities;

- Free or concessional travel;

- Sweeper, gardener, security, or domestic help;

- Interest free loans;

- Meals;

- Gifts, vouchers, tokens; and

- Club memberships.

Perquisites exempt from tax are provision of medical facilities and provision of mobile phones used by the employee for business purposes.

Allowances

An allowance is defined as a fixed quantity of money given regularly in addition to salary for employees to meet specific requirements. Allowances increase taxable income. Examples of common allowances for expatriates include:

- House rent allowance;

- Travel allowance; and

- Children’s education allowance.

Many allowances have a small exemption amount. For example, the children’s education allowance has an exemption for up to INR 100 (US$1.34) per month for up to two children.

Other allowances are fully exempt as long as actual expenses are incurred by the employee. For example, reimbursement of expenses actually incurred in the performance of an individual’s employment is exempt.

Many other exemptions exist for allowances, and taxpayers should consult with a chartered accountant in order to take full advantage of such exemptions.

Deductions

A deduction from income is available up to INR 150,000 (US$2,015) for investments in life insurance, contributions to social security funds, and tuition and fees for the purpose of full-time education at a university, college, or other educational institution.

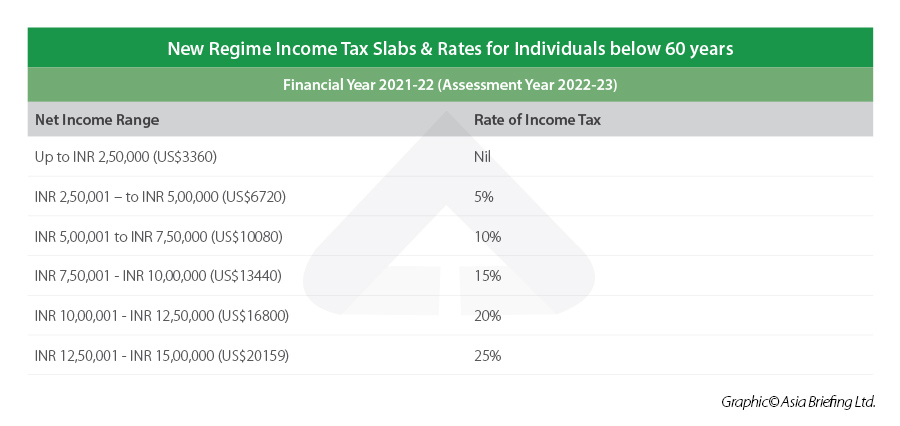

Taxation Under New Optional Tax Regime

The Finance Act, 2020 has introduced a new optional tax regime under section 115BAC, with effect from financial year 2020-21. The new regime gives an option to individuals to pay income tax at a lower rate. However, this regime does not allow individuals to claim exemptions and deductions in 70 categories, including leave travel allowance, house rent allowance, special allowances etc.

This regime is optional and salaried individuals can choose to be taxed under the new regime either at the beginning of the financial year or during the time of filing their income tax return. The individual will always have the option of switching back to the old regime every year.

In case of a non-salaried individual, the person has to choose the new regime at the time of filing the tax return. However, unlike a salaried individual, they will not have the option of switching between regimes every year. Once the person opts out of the new regime, they cannot opt in for the new regime in the future.

Non-employment Income

There are special tax rates for expatriates on income arising from non-employment sources that includes long and short-term capital gains earned on the disposal of capital assets situated in India, interests earned, and royalties payable by an Indian concern.

It should be noted that investments in shares by non-resident foreign nationals are governed by the Indian foreign direct investment policy.

Other Taxes

There is also a health and education cess assessed at 4 percent of the income tax, and applicable surcharges will be levied if the annual income exceeds INR 5 million (US$67,196).

Double Taxation Avoidance Agreements

Most expatriates worry about “double taxation” – paying taxes to two different countries on the same income. A foreign taxpayer working in India may be able to reduce taxable income in their country of primary residence (and double taxation) under a double taxation avoidance agreement.

Tax Planning

Opportunities for tax planning exist in how employers structure wages, perquisites, and allowances. In general, it is tax favorable to have expenses reimbursed rather than given as perquisites or included in wages. However, every situation is different, and foreign nationals should consult a chartered accountant to determine the best structuring of wages and benefits for their situation.

Comments